Understanding what will drive U.S.CPI (All items) over the next quarters is again becoming aboard-level question for companies that price, stock, and forecast consumer demand. In January 2026, President Trump’s administration briefly threatened a 10% tariff on imports from eight European countries (Denmark, Norway, Sweden, France, Germany, the UK, the Netherlands and Finland), with a start date reported as Feb 1, 2026. (ABC)

Trump has now backed off that immediate tariff threat following what was described as a “framework” for a Greenland-related understanding, and the plan appears paused for now. (TheGuardian) But for planning teams, the relevant point is not whether a headline is “on” or “off” today. The point is that policy risk has re-entered the demand system,and it is rational to maintain a contingency scenario for “what if tariffs are imposed anyway?”

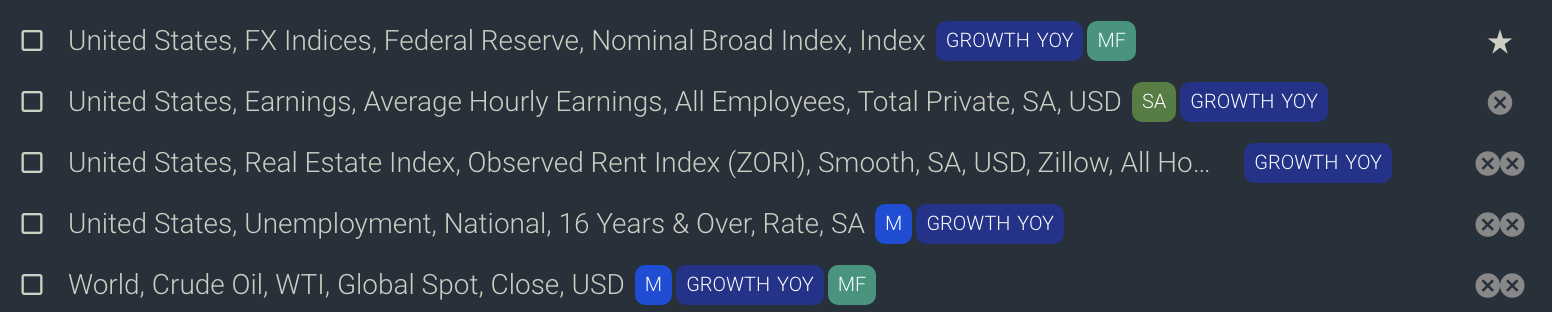

That is exactly why we built an Indicio conditional forecast for U.S. CPI, YoY, and ran a single scenario: a 10% tariff implementation path (green) versus the baseline (white). In the second screenshot, you can see the indicator panel used in the CPI model - spanning trade flows, freight, uncertainty, FX, and domestic activity - so the forecast can react to early signals before they show up in retail inflation prints.

This article focuses on the “tariffs are a tax on Americans” angle in a strictly empirical way: who pays, how fast it shows up, and how to express it credibly through one disciplined scenario.

Why “foreigners pay the tariffs” usually does not hold up in the data

Who pays first is not a debate

Under U.S. customs rules, the importer is legally liable for duties. The regulation is explicit: the liability for duties “constitutes a personal debt due from the importer to the United States.” (eCFR)

So the first payer is domestic. The “foreigners pay” claim is really a claim about economic incidence - who ends up worse off after prices and margins adjust.

Incidence: three buckets, no magic fourth option

Once the importer writes the check, the tariff wedge can only land in three places:

- Importers/brands/distributors absorb it (lower margins)

- Consumers absorb it (higher retail prices)

- Foreign exporters absorb it (lower pre-tariff prices via concessions)

For “foreigners pay” to be true at scale, you would need foreign exporters to cut prices enough to offset most of the tariff wedge. That is an empirical claim - and the last major tariff episode gives us evidence.

What empirical pass-through work says

A large literature formed around the 2018 - 2019 trade war. Two results are especially useful for forecasters.

Border pass-through is often close to complete

Fajgelbaum, Goldberg, Kennedy and Khandelwal find that prices of tariffed imports did not fall, implying complete pass-through of tariffs to duty-inclusive prices - i.e., the wedge was largely borne on the U.S. side rather than absorbed as exporter price concessions. (NBER)

Retail can lag, but the wedge remains

Cavallo, Gopinath, Neiman and Tang show tariff pass-through is much higher at the border than at the store,consistent with delayed repricing and margin compression in retail. (AmericanEconomic Association)

For CPI scenario work, the implication is practical: a tariff shock can be “real” immediately in landed costs while CPI responds unevenly over time, depending on inventory turnover, contract resets, promotions, and substitution.

A concrete example: washing machines (and spillovers)

Flaaen, Hortaçsu and Tintelnot estimate that the 2018 washing machine tariffs raised washer prices by nearly 12%, and notably dryer prices also rose by a similar amount even though dryers were not directly tariffed. (NBER)

This spillover is why tariffs often behave like a broader consumer tax: pricing umbrellas and product-line strategy can spread the impact beyond the tariff line item.

A measurement trap: why some “import price” series won’t show the tariff wedge

Another reason tariff debates get noisy is that “prices” are not one thing.

The BLS is explicit that it does not include tariffs in the Import and Export Price Indexes. (Bureau of Labor Statistics) Tariffs can still influence measured import prices indirectly (stockpiling, substitution, pass-through behavior), but duty-exclusive indexes will not mechanically reflect the duty paid at the border.

For forecasting teams, the planning lesson is simple: track the channels, not a single price series.

How Indicio turns indicators into CPI drivers

Central banks and policy institutions increasingly use conditional forecasting for scenario analysis: you fix the future path of one variable (or a small set) and simulate the joint distribution of everything else. Waggoner and Zha formalized Bayesian methods for computing full probability distributions for conditional forecasts in VAR-type systems. (JSTOR)

Indicio brings the same logic into commercial planning, but wraps it in a work flow that:

- aligns and transforms series consistently,

- runs multivariate models that capture cross-variable dynamics,

- and explains results in a driver/barrier view rather than raw coefficients.

In our CPI work, we used the indicator set shown in your screenshot panel, but we also tightened the narrative around a core set of five indicators designed to reduce collinearity and keep interpretation clean.

The updated 5-indicator CPI set

For a CPI (All items, YoY) model that stays stable under shocks, we prefer five indicators that each represent a distinct inflation mechanism:

- World, Crude Oil (YoY)

- Shelter lead: market rents (e.g.,Zillow ZORI, YoY)

- Services cost pressure: wage growth (Average Hourly Earnings, YoY)

- Trade/FX pass-through channel: broad USD index (YoY)

- Unemployment rate (YoY)

This structure avoids the common mistake of loading the model with multiple versions of the same signal (e.g., import prices + PPI + PMI prices paid all at once), which can make scenario outputs look precise but fragile.

The single scenario: 10% tariffs implemented (conditioned on FX)

Because Trump has backed off the immediate plan, the right tone is conditional: what could happen if tariffs are imposed anyway. (TheGuardian)

Scenario assumption (one scenario only)

- 10% tariffs are implemented on the targeted set of imports (as previously threatened), starting around the reported Feb 1 window. (ABC)

- No escalation path is assumed in this scenario (we keep it to a single 10% regime to avoid sensationalism).

- Retaliation and carve-outs are not hard-coded; instead we let the model reflect uncertainty through the distribution of outcomes.

Why we conditioned on FX (the broad USD index)

When you want to show “what really happens,” the key is to scenario a transmission channel, not an outcome.

Among the five indicators, FX is the cleanest scenario lever for tariffs because:

- it sits directly in the import-cost / pass-through channel,

- it is comparatively orthogonal to rent dynamics and wage growth,

- and it allows the model to determine how much of the shock shows up in goods CPI versus being muted by demand slack or delayed by pricing/inventory dynamics.

So in Indicio, we ran the conditional forecast by fixing a tariff-consistent path for the FX indicator and simulating the full CPI distribution around that path (green scenario versus white baseline). This produces a forecast that reads credibly: it is explicit about assumptions, but it does not “force” CPI to move by decree.

How to interpret the result

A credible 10% tariff scenario typically shows three features:

- The first movement is in trade-sensitive channels (FX, freight/flows, import-sensitive goods signals), not in shelter.

- CPI response is lagged and uneven, because retail repricing depends on inventory turns and competitive strategy.

- Uncertainty bands widen, because tariffs create behavioral responses (stockpiling, substitution, promovolatility) that increase forecast dispersion

If your scenario shows CPI jumping instantly and smoothly, it often meansthe model is implicitly conditioning on outcomes or overloading correlated price series.

What to watch

Even if the tariff threat is paused today, scenario monitoring should be tied to observable signals:

- renewed policy deadlines or explicit tariff implementation language,

- immediate FX moves and risk sentiment shifts,

- evidenceof pull-forward in freight/port indicators,

- early category pricing behavior (wholesale price lists, promo cadence)

The goal is not to “predict politics.” It is to keep a quantified contingency plan ready if policy risk reappears.

Closing thought

The practical takeaway is that tariffs behave less like a foreign tax and more like a domestic wedge that moves through importers, margins, and consumers, with timing driven by inventory and repricing. The empirical record from 2018 - 2019 supports that framing, and conditional forecasting is the cleanest way to turn it into a planning narrative that is rigorous rather than alarmist. (NBER)