In the high-stakes world of global supply chains, the difference between a "good guess" and a "precise forecast" is often measured in millions of dollars of excess inventory or lost sales. For decades, the industry standard has been to rely on the forecasting engines embedded within Enterprise Resource Planning (ERP) systems; most notably SAP Integrated Business Planning (IBP).

However, as market volatility becomes the new permanent, a fundamental flaw in these legacy systems has emerged. While SAP and its peers continue to rely on 20th-century mathematical frameworks, a new wave of technology, pioneered by Indicio, is finally bringing Nobel Prize-winning economic research into the boardroom.

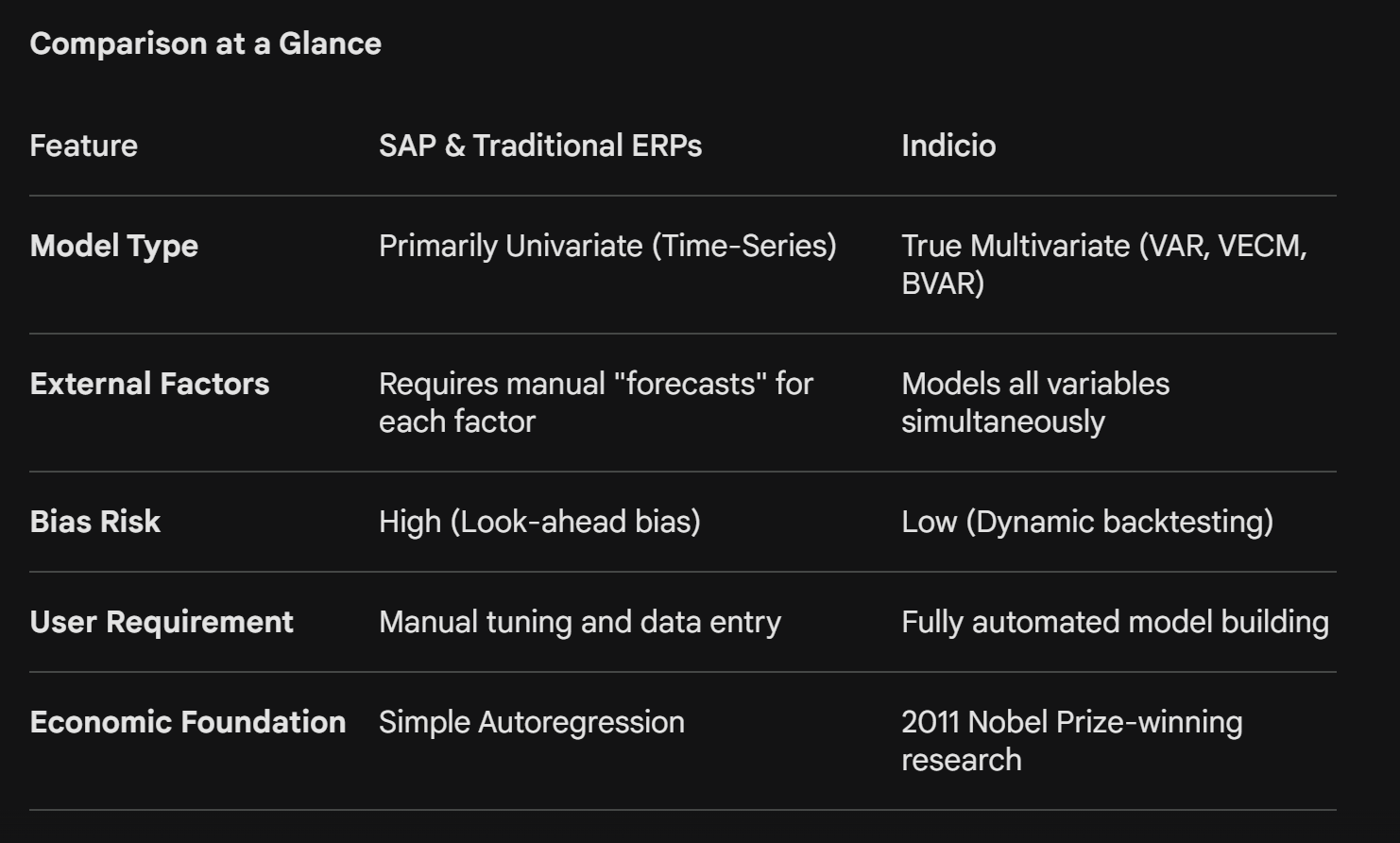

The Univariate Trap: Why SAP Only Sees Half the Picture

Most traditional planning solutions, including SAP, are built on univariate forecasting models. In simple terms, these models look at a single variable, like past sales, to predict future outcomes. They are essentially looking in the rearview mirror to steer the car.

While SAP does allow for "external regressors," factors like inflation or weather, the implementation is fundamentally flawed:

- The "Forecast for a Forecast" Problem: To use an external factor in SAP, you must first provide a perfect forecast for that factor yourself. If you want to know how interest rates will affect your sales, you have to tell SAP what interest rates will be for the next 12 months.

- Look-Ahead Bias: Because users often lack perfect future data for these external factors, the system frequently defaults to using historical data as a proxy for a "previous forecast" during model evaluation. This creates a look-ahead bias, where the model appears highly accurate during testing because it "knew" the future, but fails miserably in real-world application.

The Breakthrough: Multivariate Models and the 2011 Nobel Prize

The shift from univariate to multivariate forecasting represents the single biggest leap in predictive accuracy in the last 50 years. Unlike SAP’s approach, multivariate models treat the entire ecosystem, your sales, market trends, and economic indicators; as a single, interconnected system.

This methodology, specifically Vector Autoregression (VAR), was a breakthrough in 1970 that fundamentally changed how we understand cause and effect in the macroeconomy. The importance of this research was so profound that its pioneers, Christopher Sims and Thomas Sargent, were awarded the Nobel Prize in Economics in 2011.

"The beauty of multivariate models is that they don't just ask 'what happened?'; they model the relationship between every variable simultaneously, capturing the 'why' behind the trends."

Indicio: Democratizing the "Impossible" Model

If multivariate models are so superior, why hasn’t every company switched? Historically, the barrier has been complexity. These models require an elite level of expertise to set parameters, hyperparameters, and Bayesian priors. Without a PhD in econometrics, a VAR model is almost impossible to tune correctly; often leading to "overfitting" or total model collapse.

Indicio has changed the game by automating the "Expert-in-the-Loop."

By using advanced machine learning to handle the heavy lifting of parameter selection and model pooling, Indicio makes Nobel-caliber multivariate forecasting available to any decision-maker. You no longer need to be a statistician to account for GDP fluctuations, consumer price indices, or regional economic shifts.

Moving Beyond the Spreadsheet

The reality is that your business doesn't exist in a vacuum. Sales are influenced by the economy, which is influenced by policy, which is influenced by global events. Continuing to use a univariate model is like trying to solve a 3D puzzle with a 2D map.

Indicio provides the 3D map. By automating the most sophisticated models in economic history, it allows companies to stop reacting to the market and start anticipating it.

Would you like me to help you draft a specific case study proposal to show your leadership how Indicio’s multivariate approach could reduce your specific forecast error?