The VARX Endogenous-First model is an extension of the VARX Lasso model (see Advanced: VARX Lasso) which instead of a regular Lasso penalty is using a Group Lasso penalty, grouping the coefficients in the equation per lag in the model (for details see the article Advanced: VARX Lag Group Lasso). The VARX Endogenous-First model penalty is also constructed in such a way that at each lag, endogenous variables are prioritized over exogenous ones. This means that for an exogenous variable to be able to have an effect at lag ll, the endogenous variables at the same lag must also have one.

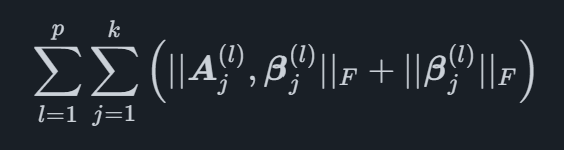

In the case of no exogenous indicators, this model reduces to the VARX Lag Group Lasso, why it is not built when there are no exogenous indicators or events present in the data. Mathematically, the penalty can be written as

where ∣∣X∣∣F is the Frobenius norm mentioned in the VARX Lag Group Lasso article. The coefficients for the endogenous indicators at lag l are denoted A(l) and for the exogenous as β(l). This penalty structure is useful for selecting a per variable lag order in a setting where the endogenous variables are considered more important than the exogenous ones.

We provide automated forecasting software that blends cutting-edge academic methods with market-specific leading indicators. This helps your organization reach the highest level of forecasting accuracy.

© 2025 Indicio Technologies All Rights Reserved