The VAR Weighted Lag Lasso model is an extension of the VARX Lasso model which increases geometrically as the lag order increases. This has the effect of penalizing higher lags more than lower.

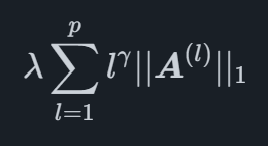

The weighted lag lasso penalty can be written as

where γ is a second hyperparameter which determines the shape of the increased penalty for the higher lags. The intuition behind the penalty is that for a series which is affected more by recent developments than developments further back, the coefficients further back should be penalized more heavily.

We provide automated forecasting software that blends cutting-edge academic methods with market-specific leading indicators. This helps your organization reach the highest level of forecasting accuracy.

© 2025 Indicio Technologies All Rights Reserved