The HVAR Componentwise Lasso model is an extension of the VARX Lasso model (see VARX Lasso) where a special hierarchical penalty is used. This penalty offers not only regularization to avoid over-fitting in terms of shrinking parameters towards zero, but also automatic selection of maximum lag order.

The HVAR Componentwise Lasso model allows selection of lag order per variable equation. Different variables in a VAR system may exhibit distinct temporal dependencies. Allowing variable-specific lag orders accommodates variations in the speed at which different variables respond to past values of themselves and other variables. This enhances the model's ability to capture the unique dynamics of each variable.

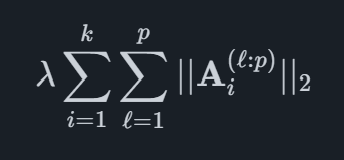

Mathematically, the penalty structure is defined for k variables and a maximum of p lags as

where each term in the inner sum contains the p−l+1 matrices corresponding to lags l,...,p.

We provide automated forecasting software that blends cutting-edge academic methods with market-specific leading indicators. This helps your organization reach the highest level of forecasting accuracy.

© 2025 Indicio Technologies All Rights Reserved